A Brilliant Sunset For One Market's Early Days

A Brilliant Sunset For One Market's Early Days

(On Crypto)

Investing in virtual assets is venture capitalism. It’s a quest to build the future, and replace the present. Everything is early and imperfect, and is being developed by trial and error.

Investing in virtual assets is venture capitalism. It’s a quest to build the future, and replace the present. Everything is early and imperfect, and is being developed by trial and error.

Everything new begins with a crack in the firmament, a shifting of the current order’s tectonic tensions, nudging forward a tide of ebullience stretching into the sky. A wave comes in and some are riding it to shore, ready for garlands. Others will be pulled under.

I noticed the following charts about prices in that most speculative of markets: the future. They are not the most comprehensive, complete or most accurate of predictions about what is to come in fintech, startups or virtual assets. This is a launching point for today’s Layer 2 review about one aspect of the future, its financing at the moment.

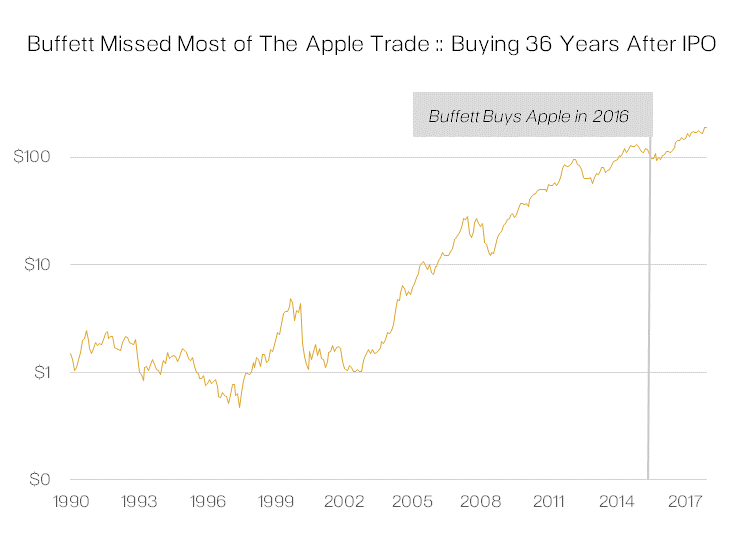

Dan Pantera, of leading cryto investment firm Pantera Capital, in the firm’s June 30, 2018 letter, playfully poked at Warren Buffett’s assessment of bitcoin, and teased that if Buffett were to belatedly invest in bitcoin much in the same way Apple was invested some 36 years after its debut, then it would be at a hefty price, sometime in the year 2045.

(Chart from Pantera Capital’s Letter, June 2018)

With that said, Pantera is not all roses and sunshine. Even the firm quoted founder Dan Pantera at the Consensus 2018 event as saying: “ICOs are overhyped. People think you can do a token sale on any venture backed company without really figuring out what fundamental purpose the token serves. The token absolutely MUST function.” (via PanteraCapital, 10:09 AM May 15, 2018)

Tren Griffin, through his entertaining and instructive site, had a post which comes to mind, entitled “A Dozen Things You can Learn from Biggie Smalls (The Notorious B.I.G.) About Business”. Griffin observed, “A founder who is focused on making products people want to buy will succeed far more often than founders who are mostly concerned with things like getting prime speaking slots at major industry conferences or having a hip office with exposed brick walls and water views.” This was his interpretation of Biggie Smalls line “If y’all love the music, y’all gonna buy the music.”

But venture capitalism is associated with the new and with innovation. In that same post Griffin acknowledges this with another line from Biggie: ““Your style is played out, Like Arnold and that, what you talkin’ bout Willis.” Griffin’s interpretation is: “In other words, a person or business should avoid just repeating what others have done if they want to produce a substantial and valuable innovation. The cultural reference in the Biggie quote is to a Garry Coleman (AKA Arnold) tagline from the TV show Different Strokes that repeated itself perhaps a bit too often.”

What fundamental purposes would be served by a valuable innovation which could be met by a product people would want to buy? (h.t Dan Pantera, Tren Griffin and Biggie Smalls) SEC Corporate Finance Director Bill Hinman made some relevant remarks, at the June 14, 2018 Yahoo Finance All Markets Summit as part of a great speech about the role of U.S. Federal securities regulation in this space:

“[L]et me share what I believe may be most exciting about distributed ledger technology — that is, the potential to share information, transfer value, and record transactions in a decentralized digital environment. Potential applications include supply chain management, intellectual property rights licensing, stock ownership transfers and countless others. There is real value in creating applications that can be accessed and executed electronically with a public, immutable record and without the need for a trusted third party to verify transactions.”

“Some people believe that this technology will transform e-commerce as we know it. There is excitement and a great deal of speculative interest around this new technology. Unfortunately, there also are cases of fraud. In many regards, it is still “early days.”

Two recent deals during these early days involved big names: Binance and Kik.

First up is Binance’s deal with a crowd-funding platform spun off from Angellist- Republic. To my recollection, Republic was formed originally to meet the needs of the investment space created with the passage of crowdfunding legislation. The exclusive June 8, 2018 coverage from Coindesk:

“Republic, a crowdequity platform that can help ICO issuers manage token sales that was spun out of AngelList, has raised $12 million in commitments for a token presale….Led by Binance Labs, the investing division of cryptocurrency exchange provider Binance…(Investors purchased both the new crypto token and equity in the company.)…[as] part of Republic’s interest in ultimately raising as much as $92 million total selling its crypto token, with a yet to be announced public sale.”

“According to Republic co-founder Kendrick Nguyen, the [Republic] token will be used to incentivize users to take an active interest in their investments, by allowing Republic to potentially provide access to ICO deals and offer a share in the revenue earned by the company as it grows.”

“We will be doing a combination of Reg D, Reg S and Reg A+ to make sure our tokens are widely available, irrespective of income or net worth in the U.S. and beyond…” said Nguyen.

It appears that Republic wants to use a hybrid of both “SAFE” and “SAFT” financing, calling it “SAFEST” (short for “Simple Agreement for Future Equity and Security Tokens”), which have partial convertibility into Republic equity during a a “pre-sale” and full convertibility if no tokens are issued. Coindesk noted that both the whitepaper and the actual Republic tokens have not yet been released at the time of their reporting. One cautionary precedent for the Binance-Republic agreement could be what became of messaging platform Kik’s 100M USD 2017 fundraising. Kik CEO Ted Livingston seemed somewhat sanguine post-fundraise.

Early days. There is a nice summary by finance professor Stephen McKeon on “The Security Token Thesis”, which provides a historical analogy of this financing technology: “The current stage of security tokens is analogous to broadcasting a radio program on television. We’ve just begun to tap the expanded design space for securities that it facilitates. It will be a huge canvas for creativity over the next decade for those involved with security creation.” The trendy word used for this has been “tokenization”. Meanwhile, what have professional investors been doing?

Recode’s Theodore Schieffler has provided a breakdown on what incumbent VCs are doing, in its June 21, 2018 piece, “Why are big VCs opening crypto funds”:

“So nearly all of the top tech investors over the last year have been meeting internally and reviewing documents to assess how they can equip themselves legally and financially to invest in ways that don’t fit with their traditional business model.” Schieffler’s top-down is the VCs may be either launching a pure crypto fund (e.g. Andreesen Horowitz), “earmark” from a pre-existing fund (Lightspeed Venture), invest in others (Union Squre Ventures deal with Multicoin Capital), or stand pat with a few legal tweaks (DFJ).

Just as some valuations are adjusting, older deep pockets are making plans, and figuring out how to adjust their models past shoe-horns and bolt-ons. Here’s some timely June 20 comments from Union Square Ventures (USV) on this:

“[T]he venture capital fund model is not optimized for investing in the blockchain/crypto sector. Blockchain/crypto companies/projects often finance and monetize via tokens which can become liquid quickly and thus we can end up holding highly liquid and volatile positions which is not something we have traditionally done. And because USV operates under the venture capital exemption to Dodd-Frank, we are limited to 20% of our holdings at cost in “non-qualifying” investments, which include tokens.”

It’s not that the firm has plans to be a “fund of funds” but the value comes from the idea that “[y]ou can make a lot of money by being right about something most people think is incorrect. So at USV, we appreciate and value original thinking.” As a result their approach has been to take their deep pockets and patiences to invest in a bundle of crypto funds with deep thinkers.

Let’s return to SEC director Hinman’s remarks, with thoughts of Republic and what VC firms are figuring out what to do, since many business models are defined and confined in part by U.S. federal securities regulations:

“I will begin by describing what I often see. Promoters, in order to raise money to develop networks on which digital assets will operate, often sell the tokens or coins rather than sell shares, issue notes or obtain bank financing. But, in many cases, the economic substance is the same as a conventional securities offering. Funds are raised with the expectation that the promoters will build their system and investors can earn a return on the instrument — usually by selling their tokens in the secondary market once the promoters create something of value with the proceeds and the value of the digital enterprise increases.”

“When we see that kind of economic transaction, it is easy to apply the Supreme Court’s “investment contract” test first announced in SEC v. Howey. That test requires an investment of money in a common enterprise with an expectation of profit derived from the efforts of others.”

Here is a link to an earlier piece quoting Hinman’s explanation of the fact pattern of SEC v. Howey.

“The digital asset itself is simply code. But the way it is sold — as part of an investment; to non-users; by promoters to develop the enterprise — can be, and, in that context, most often is, a security — because it evidences an investment contract. And regulating these transactions as securities transactions makes sense. The impetus of the Securities Act is to remove the information asymmetry between promoters and investors.”

[However,] “simply labeling a digital asset a “utility token” does not turn the asset into something that is not a security. I recognize that the Supreme Court has acknowledged that if someone is purchasing an asset for consumption only, it is likely not a security. But, the economic substance of the transaction always determines the legal analysis, not the labels.”

Aaron Wright, Esq., Cardozo Law professor and Director of the Cardozo Blockchain Project provides some granularity about the significance of SEC director Hinman’s remarks (from a threadreader app’s compilation of Prof. Wright’s June 18, 2018 commentary), which helped to explain why the price of Ethereum had experienced a brief price rise during that speech:

“[T]he speech is notable because Hinman is the Director of Corporation Finance at the SEC, the part of the SEC generally responsible for policy related questions — particularly as they related to public markets.”

“It’s also important to recognize that the speech is not legally binding.”

“As framed by Hinman, “where purchasers would no longer reasonably expect a person or group to carry out essential managerial or entrepreneurial efforts” the sale of the token at that time may not implicate securities laws.”

“The speech indicated that there may be other networks that become sufficiently “decentralized” where regulating the tokens as securities may not be required.”

“As framed by Hinman, “where purchasers would no longer reasonably expect a person or group to carry out essential managerial or entrepreneurial efforts” the sale of the token at that time may not implicate securities laws.”

“[T]okens network that were at one point in time “decentralized” could “centralize” and fall under the scope of the securities law regime. (Consider what this means for Ripple or if another fork of Bitcoin that consolidates it operation further.)”

“The speech did not provide much guidance as to what “decentralization” means outside of the above. My sense is that these questions will clog courts for years as part of litigation. We’ll probably only gain clarity in 5 years or so as these litigations wind their way through district and Circuit Courts.”

“Due to these risks, Hinman notes that many in the industry ‘are beginning to realize that, in some circumstances, it might be easier to start a blockchain-based enterprise in a more conventional way’…”

“In other words, conduct the initial funding through a registered or exempt equity or debt offering and, once the network is up and running, distribute or offer blockchain-based tokens or coins to participants who need the functionality the network and the digital assets offer…This allows the tokens or coins to be structured and offered in a way where it is evident that purchasers are not making an investment in the development of the enterprise.”

Marco Santori,Esq., President of, and Chief Legal Officer for, Blockstack also reviewed SEC Director Hinman’s speech (threadreaderapp used to compile Mr. Santori’s light-hearted analysis). (Note: Mr. Santori is also one of the creators of the SAFT investment vehicle.):

“The Ether token, according to SEC, is not a security. The Ethereum Foundation’s sale of Ether, on the other hand, almost certainly was a security (SEC didn’t say that last part explicitly but pretty much laid it out).”

“As it’s now commonly understood: The contract between Howey and the investors was a security, but the oranges were not a security. The oranges had a consumptive, functional use (a yummy one).”

(The Howey case centered on an orange growing business.)

In contrast to the relatively ebullient interpretation by Mr. Santori, Mr. Preston Byrne, Esq. has a more conservative assessment:

“Where I struggle is in understanding how tokens issued by a scheme start life as investment contracts, and then, because the scheme successfully evades enforcement action for 4 years, the tokens issued by the scheme somehow lose their character as investment contracts.”

“If we assume for the sake of argument that the Howey criteria are met, and if we pay very close attention to the word “scheme” in Howey’s “contract, transaction, or scheme,” it seems clear that later decentralization should not save a cryptocurrency scheme from earlier transgressions; where the later-mined tokens are part of the same scheme as the presale coins and facilitate its objectives, and it was an investment contract at inception, then as a practical ma_er the Ether sold in the presale and the Ether today are all part of the same scheme, albeit one that has achieved completely its promoters’ original goals.”

There is more of interest, particularly about decentralization, in his note. Let’s return one of the last words on this sub-topic.

SEC Chairman Clayton defined this view of how the economic substance of transactions defines what is a security via a recent June 8 CNBC interview: “A token, a digital asset, where I give you money and you go off and start some venture…and in return for giving you my money, you say, You know what? I’m going to give you a return, or you can get a return in a secondary market by selling your token to somebody. That is a security and we regulate that. We regulate the selling of that security and we regulate the trading of that security. That’s our job, and we’ve been doing it for a long time.”

This marks a shifting not of technology but of regulatory awareness and comes after a heated speculative environment in these virtual assets.

The sentiment in financing has also shifted. There’s a great piece by Ari Paul which interested observers hopefully have read or will read. The following are excerpts from an internal note which Paul wanted to share with the public. In summary, Paul’s assessment of the market is “We’re seeing something play out in real time (but slow motion) that we’ve long expected. The crazy valuations of early stage projects are falling to earth.”

“In the last 6 months, the exchange buyer has consistently been losing badly, so they’ve mostly stopped buying. This means that the late stage pre-ICO investor also started often losing. Until now, the early stage pre-ICO investor was still winning, but it’s like dominos, and we’re nearing that last domino falling as well.”

He observes that even with the deep discounts offered, perhaps only traders, or those with a traders’ mentality, would be responsive. Investors, whose mindset might not be dissimilar to venture capitalists, would be averse to such “bargains”. What follows is another natural human aversion to confronting the reality of mark-downs. Not all VC deals are going to exit with a heroic multiple.

Here is some artful phrasing by Paul, which I will someday steal for future use:

“This market dynamic is not a surprise to most of the investors in the space — many understood that they were playing musical chairs, and just hoping to be able to find a chair before the music stopped. Timing the music is far harder than identifying the game.”

He ends with advice which both Buffett and Pantera would agree to: first, be realistic. second, think about what you really need. third and last, love your investors. Please take a moment if you’re an investor to read Paul’s note.

This current downbeat ICOs mood is not completely reflected in the more conventional equity markets for IPOs. Barrons recently observed in Alex Eule’s “Why IPOs Are A Boom, Not a Bubble”, on June 23, 2018, that the current IPO market, while festive, is not quite like the one from almost 20 years ago. Barrons’ Eule observed, “The largest Unicorns remain stuck in the barn. And the numbers are being driven by a wide range of companies, not prototypical Silicon Valley startups. Just 27% of IPOs in the last 12 months came from tech, says Renaissance, trailing №1 health care, driven by a wave of biotech debuts. Tech’s IPO share has hovered around this level for the last few years; in 2011 it was 44%, according to data from University of Florida professor Jay Ritter. In 1999, tech made up 78% of all IPOs.” And in a way this makes sense, the private markets have provided both the capital and patience to hold and trade between themselves. There has been little need or urgency for the newest tech companies to go public.

As for equities long past their IPO youth, FT’s John Auther’s update on the status of the most successful of tech public companies, a/k/a the “FANGs”, continues to confirm just how narrow the action is, and how sharp Mr. Market’s focus is:

“I took the Fangs to be Facebook, Amazon, Apple, Microsoft, Netflix, Nvidia and Google. According to a few calculations I made on the back of an envelope (or more precisely, with a Bloomberg terminal and a spreadsheet), the market cap of these seven stocks has risen by $772bn so far this year. Meanwhile the market cap of the S&P 500 as a whole has risen by $673bn. Excluding just those seven Fangs takes the S&P from a 2 per cent gain for the year to a slight loss.”

Closing thoughts: These are exciting times. So much capital and attention just within the confines of investing in the future. Every deep pocket filled to the brim, overflowing and still ready for more but where will it be deployed. It arrives in a frenzy and then leaves. Where will these pockets go to next and what’s going to happen as more regulations and case rulings happen? I think the sun has set on this first phase, these sunny early days, of raising money without worry as to what investors ultimately purchased with their capital. It’s not the end however. The sun rises again, and the new day will be greeted with more professional investors and regulators.

Originally published at big-stack.com on June 24, 2018.