On Private Companies, Electric Cars & Bizarre Bonds

(Wimpy Burger Finance, Part 2)

“Reality provides us with facts so romantic that imagination itself could add nothing to them.” ― Jules Verne

There is a raging planetary party going on in crypto-space. In the meantime, investors in both startups and sovereign debt are facing basically the same question. Bond investors wonder whether or not they will be paid back next Tuesday for burgers they paid for today. Startup folks hope their moon-shot project makes it to the launchpad, off the ground and leaps into deep space.

It used to be that the big finish for a startup was an IPO, getting acquired/acqui-hired, rolled-up, or in many cases, reluctantly closed down with a liquidator’s help. The big win was liquid public share or fiat cash.

Now, it seems all a Unicorn has to do is look for a big sovereign wealth fund, Softbank or even a mutual fund complex, that is ready to scuff their All-Birds (or limited edition sneakers with perfect colorway) with some late stage tire-kicking. As to whether this is diworsification or diversification, what’s the difference when you can tout founder can-kicking as pension fund tire-kicking ? And, speaking of Softbank, you can ask the folks at Uber what’s a down-round amongst friends?

And what about those companies which do make the leap and go public? Some of them have gone on to glory, including the “FANG” group of companies (Facebook, Amazon, Netflix and Google). These rockets have launched and gone into deep space, headed for another star system. There has been one company, that has been a candidate for this exclusive club of moon shots and there are both fans and critics debating and making their bets accordingly. Tesla.

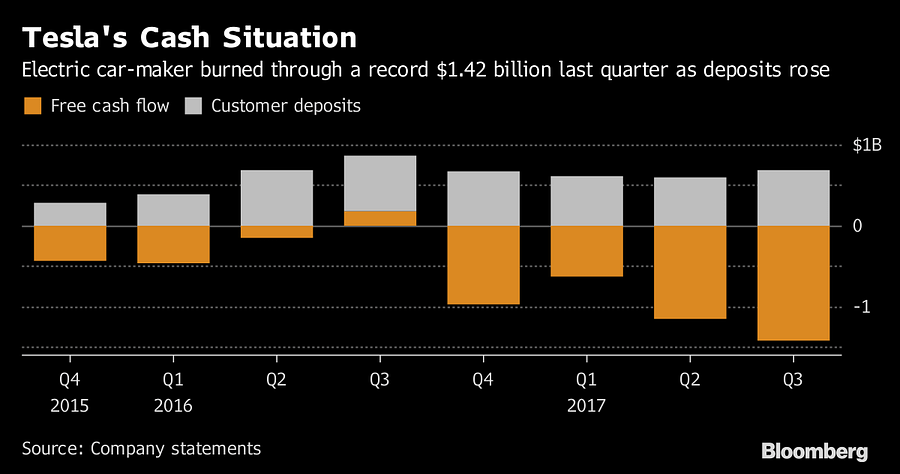

Tesla continues to astound and confound. It has transformed the automotive industry and triggered a sea change in strategy and cap-ex. Electric cars were the stuff of science fiction and a very narrow market segment. Now just about every manufacturer is doing likewise. The doubt isn’t about whether or not many of our next cars will be electric but whether or not most of them will be made by Tesla. Specifically, I refer to customers’ cash to burn today for cars that will be delivered…eventually.

It’s not unusual to raise current dollars to pay for future production but this looks different. But it’s like Tesla’s reservation and deposit list, as a financial instrumentality will be the most memorable source of cheap financing since Warren Buffett’s use of “float” from his insurance operations, with Tesla’s access to financing straight from its fans.

Yes, it’s true that many businesses’ operational cash are financed by their customers (like those New Year’s resolutions leading to those gym membership fees being charged every January 1). In fact, it looks like a lot of media is remembering that old fashioned subscriptions might be preferable to advertising. Fancier examples of such financing includes SAAS businesses, which ultimately helped Salesforce put up a very tall beautiful building above in San Francisco. The question which follows is about delivery, payback, and payoffs from all of these promises on paper. This same question faces another group of investors — those in sovereign bonds.

There are a couple of interesting promises in this old corner of the markets:

We have 1000 year bonds on deck in Northern Europe. That’s way past next tuesday.

We have 3 year bonds with negative yield. It’s like Wimpy got a “Happy Meal” (Burgers, fries, drink & maybe a toy) but all he owes is the price of the burger.

But that is small change. We have a Treasury Secretary who appears to have no forward view of inflation and is willing to lean in and borrow a bit heavier on the short end of the curve. Now that’s quite a promise with the biggest market of them all. At a global aggregate value above $35+ TRILLION USD, according the Bank of International Settlements, the total global government bond market could tell both startup/new tech “story” companies (at 750+B to $1T USD) and crypto assets (at about $350+ to $500 B USD market cap) “to hold its beer”.

The hat trick of raising money today for promises of tomorrow is not just confined to future virtual goods. This is at the heart of capital markets. This was how this country was built in part. Continentals. Canal bonds. Railroad bonds and shares. Steel, petroleum, automobile, radio and airplane stocks. Something today for something new and spectacular tomorrow. When it works, it’s like the Fourth of July and New Year’s Day all wrapped in one.

And step by step we have added to the menagerie of promises between the present and the future.

(This zoo has included the following: Go Go 60s story “letter” stocks, index futures, index funds, “stocks of mutual funds” a/k/a ETFs, futures on stocks, “stocks of futures” a/k/a ETNs, options on everything, friends & family (as always), angels, pre-seed, seed, A series, B series, etc., don’t forget insurance, reinsurance, CDOs, hedge funds, fund of funds, repos, leasebacks and more.)

Not every Jules Verne moonshot project makes it off the ground or even makes it to the launchpad. In the end of his book, Verne’s astronauts did launch into space, where a lot of things went wrong along the way, but they made it home.

And so, there will be bond deals that help keep the ship of state sailing forward, there will be crypto assets that will deliver some kind “utility” as promised, and there will be “Unicorns” that will improve living standards for perhaps billions. But which ones? Which moonshot makes it back home and which were duds?

Why do this? Because, some of the moon-shots do make it to the launch-pad, launch, reach escape velocity and come back home. The world is never the same again afterwards, but in a good way. It happens all the time. This is what keeps us coming back. There are crash & burn disasters along the way but the ones that stick the landing keep us coming back. (In case you’re thinking about SpaceX, here’s a link to a cool video.)

More on The Big Stack: The Intersection Between History, Trends & Tech

Originally published at big-stack.com on November 28, 2017.