P is For Peloton and The PAULSs

PAULSs the 2010s Challenged Sequel To the FANGs

The PAULS Come Home With Peloton

The “PAULSs” are the 2010s sequel to the 1990s/2000s era “FANGs”.

The PAULS stand for: $Peloton $AIRBNB $UBER $LYFT $SLACK

What the PAULSs have in common is that they were all massively funded startups sheltered from the requirements facing publicly traded companies. They are startups, with sharing / on-demand business models, which have been private for most of the 2010s. They’re now finally going public.

Honorable members of the PAULS include Postmates And Pinterest.

So many “Ps” this time! You could include Pinterest but it feels like a different cohort. It’s more of a social network like Facebook.

Peloton was founded by John Foley in 2012. He enjoyed working out with an instructor so much more than exercising alone that he wanted to bring it into millions of homes.

Peloton used Kickstarter crowdfunding and a 3.5M Series A round to fund $2K+ exercise bikes with a $39 monthly subscription to influencer instructors. It’s one part Netflix and one part online classes.

Peloton Kickstarter Bike (297 backers pledged $307,332 to help bring this project to life)

These long awaited IPOs are the latest phase of “The Big Stack”, an era driven by two trends: one financial and the other tech-based.

First we have a QE-fueled post-”Big Short” era of easy credit.

Second, a massive and continuous fall in tech infrastructure costs.

Back in the 90’s companies had to go public as fast as possible to get the capital they needed.

Amazon was founded in 1994 and then went public in May 1997. This is very different by today’s standards. Startups have enjoyed access to lots of money and lots of time while staying private over the past decade.

The past decade’s financial environment has allowed these startups to stay private for far longer than Amazon did, and funded a hypergrowth of expenses, headcount and ambition.

Peloton had a “Series F” that raised $550M for $4.15B valuation — that’s the kind of fuel that’s been available for staying private for longer.

The PAULS are internet businesses which would have been impossible to build in the 1990s -- never mind fund and keep private for nearly a decade. This is what created “Unicorns” — $1B+ USD private companies that were still considered “startups”.

There are about 400 such Unicorns that have raised about 300B USD with a total “valuation” of 1.2T USD. The PAULS are among the most well known “Unicorns” to Western investors.

A tweet from reporter Leslie Picker wryly summed up the Peloton IPO:

The Peloton S-1 reads like a list of income statement “line items” strung together. And of course it begins with the word “tech”.

What bothers me about how Peloton describes itself first as a “tech” company is that it reads like marketing “buzz”. Let’s break it down.

Peloton’s has two core businesses (when you take away the “buzz” of its branding): hardware (those sexy bikes photographed in luxurious apartment settings) and membership subscriptions.

There are also internal businesses like design, apparel, and logistics. They might be described as “modules”, ala Ben Thompson’s Stratechery — parts of a business model.

Each of these parts of Peloton’s business could be stripped away via competition, spinoff or obsolescence over the coming years. Why do I mention this?

One example of this is what happened with the old internet site “Craigslist”. Craigslist had categories for selling your old stuff, dating, and so on. Each of these were “modules” which another startup would eventually take over. Competition and obsolescence ate into its value.

Peloton’s various modules are vulnerable to competitors.

EVERY company wants to say it’s a “tech” company but that’s an overused buzzword.

Saying something is a “tech” company in 2019 is like 19th calling something a “.com” company 20 years ago or “Blockchain” or “Cannabis” company today.

Ben Thompson had an interesting analogy for Peloton: “It is basically the Netflix of exercise attached to a $2,000 set-top box.”

We have read so many startups describing themselves as the “Uber” of something but to use Netflix is interesting. Netflix is the ultimate couch potato platform isn’t it? It’s like saying “it is basically the couch potato platform of exercise with expensive hardware”.

Jokes aside, the analogy refers to on-demand usage with hooks to get the user to spend more time on a Peloton (classes and that group feeling of being in a cohort).

Just how has this tech company been doing? Keep in mind that it was founded in 2012.

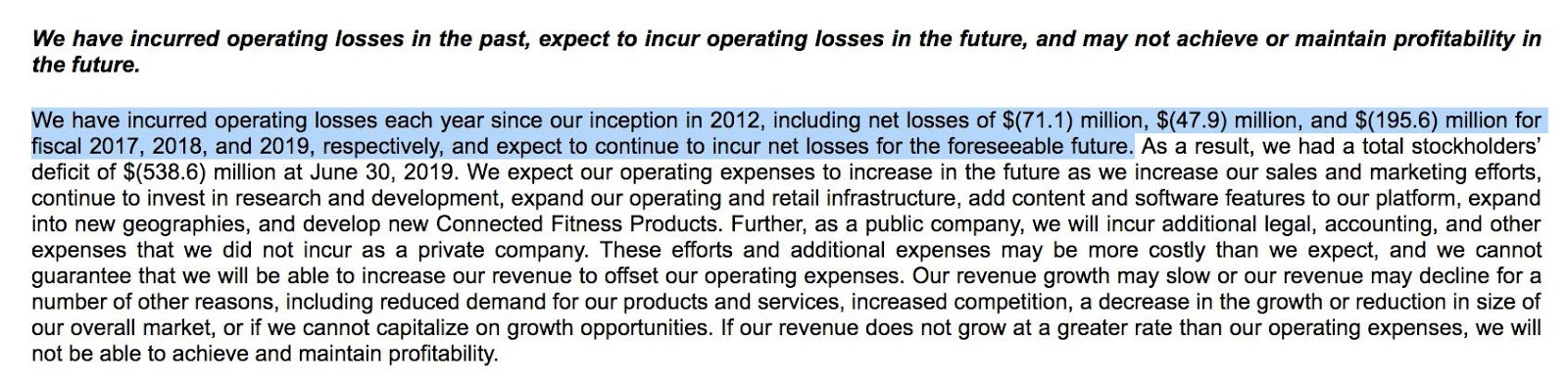

Peloton revealed IPO documents showing widening losses of $245.7 million on sales of $915 million.

“In the fiscal year ended June 30, 2019, Peloton reported sales grew 110% to $915 million from $435 million in fiscal 2018. Meanwhile, its 2019 net loss widened to $245.7 million, from a net loss of $47.9 million in the prior year.

...

the company also said it has “identified material weaknesses” its its internal control over financial reporting, which it had not fully addressed as of June 30, 2019. To address the problem, it is adding more qualified personnel.”

It is anticipated that its IPO will raise $500M on an $8B USD valuation.

This is a startup which has been operating for nearly a decade. It reported a widened “net loss” of nearly a quarter of a billion dollars and still has problems with its internal financial reporting. Is $8B USD a realistic value? Profitability is an issue.

Contrast that with this statement a year before by the CEO asserting Peloton’s profitability.

“Weirdly” is an interesting word to use given Peloton’s admission that it needs “more qualified personnel” for financial reporting.

One counter to the profit worry is an impressive sounding subscribers count - from CNBC:

“Its connected fitness subscriber base — or users with a paid subscription or one that has been paused for up to three months — rose to 511,202 in 2019 from 245,667 a year ago. The company boasts 1.4 million members, which it defines as any individual with a Peloton account.”

Is there an argument to justify the narrative, the valuation, and Peloton’s “burn rate”?

Ben Thompson elaborates in his piece, “Privacy Fundamentalism Follow-up, Peloton’s S-1, Peloton and Disruption”:

“is Peloton a hardware company or a subscription service? Interestingly, the founders originally wanted to be the latter: Peloton started out selling bikes at cost with the idea of monetizing solely through subscription revenue, but according to Peloton CEO John Foley their target customers — at that time primarily spin class attendees — were put off by how “cheap” the bike was. So they raised the price, which means Peloton is both.”

Thompson nails down Peloton’s earnings issue with the argument that “the ultimate profitability comes down to just how sticky that subscription service is”.

He acknowledged that while Customer Acquisition Costs (CAC) did go up, the newer customers are more engaged, meaning lower churn. We will see if that’s enough, “tech” or no tech.

An impressive analysis by Babak Azad offered the good, the bad and the ugly on Peloton’s numbers. Azad calculated that Peloton’s customers were acquired for essentially “free”, with the cost covered by sales of hardware.

In his broader analysis of Peloton’s S-1, he was not convinced by the company’s use of just subscription numbers for the Lifetime Value (“LTV”) of Peloton’s customers:

“I’m a massive Peloton fan myself but there’s no way I can conceive of being a subscriber for 13 years. Now, it’s highly possible that they generate the same amount of money from me and other subscribers over a shorter period of time, but using 160+ months as the expected lifetime is, well, not believable. Now, they don’t actually say 160 months – they just describe the calc. But that’s what it’s based on…. customers who were acquired in 2019 are expected to generate over $1 billion in revenues over their lifetime. Over 13 years. Um, ok.”

Peloton recently launched a line of for runners and joggers — “Tread” — with $4K+ treadmills.

The Azad analysis thinks it won’t be conversions from bikes to treadmills that helps Peloton boost revenue enough to become profitable, but apparel and supplement sales. Revenue from apparel and supplement sales are currently small but they could be a big future source of substantial revenue growth. Azad acknowledges the fandom, customer experience, and increasing workouts - the love is real.

“a massive number of customers. Of fans. Of devotees.

Of customers who will fly from wherever they live to do their anniversary ride in the NYC studio. Hopefully with their favorite trainer. And snapping a pic while they’re at it.

Of customers who love that they can click a button on their screen when a favorite song plays, and that song sync’s with their Spotify account.

Over the past few years, they established a foundation of half of a milliion loyal paying customers. That’s a very very asset to have created.

What happens when the market turns?”

In summary, Azad believes it’s Peloton’s large extended “family” of 500,000 users that must carry the company through any future economic downturn. We will see.

Peloton is not the only “PAUL” going public with a huge valuation outpacing revenue.

Of the PAULS companies going public, there may be one bright spot in terms of financial performance. I read that Pinterest had relatively good financial results. Aswath Damodran, “the dean of valuation” from NYU, looking at Pinterest, Uber, Lyft and video service Zoom found the valuations to be high but believed Pinterest had “a pathway to profitability”. You need the word “tech” if you want to get the valuation, whether or not there was a path to profitability.

By the time the 2020s are in the books, maybe we’ll remember the latest startups as:

Riding bikes indoors, but you’re not alone

Living in someone else’s home or working in someone else’s building

Riding in someone else’s car

Working with people non-stop alone but not alone,

But because it was fueled on someone else’s money (i.e. VCs), we had to say “tech”.

The pressure is on to justify all that capital and all that fundraising. Maybe it’ll work out.