Streamland vs. The Magic Kingdom

(On Netflix and Disney Business Models $NFLX $DIS)

I. How A $40 Late Fee Leads Me To “Halt & Catch Fire”:

I recently rediscovered a series about startups on Netflix which is likely to become a cult classic — a 1980/90s drama called “Halt & Catch Fire”. Interlaced within the dramatic arc of this 80s/90s tech & music nostaligia-fest were familiar themes about innovation and disruption. During a bingewatch I paused it in search of other content — one thing leads to another (i.e. how come there’s only one Avengers flick available?) and I began to think about Disney. There is another drama unfolding in front of us, a really big one, unfolding between Disney and Netflix.

What if Reed Hastings hadn’t been hit with $40 late fee for his DVD rental of Apollo 13 from Blockbuster Video? The address of the Blockbuster where Hastings was inspired to solve a pain point should be bought by Netflix and enshrined as the birthplace of “Streamland”.

Over the past 20 years, Netflix has grown from one man, trying to avoid trouble with his spouse over a $40 rental late fee, starting a DVD rental by mail business (which in its early days had a catalogue of 900 movies) into a global platform with 125 million subscribers. At its most recent quarterly earning report, Netflix added 7.4 million subs (of which 5M were international) topping analyst expectations by 0.8M. The scale of this platform’s growth stuns.

Netflix’s power law growth seems to exemplify the flywheel narrative of the best internet platforms. But there might be some re-writes to this story coming, including the addition of a new cast of characters to join the streaming plotline, featuring Disney. Recently, CEO Bob Iger affirmed that the Magic Kingdom was going to stream its content exclusively.

A fascinating talk between Scott Galloway (Professor at NYU, author of “The Four”, and founder of L2) and Derek Thompson (Author and Editor at The Atlantic) provided a top-down view of what we may expect at Disney. I particularly appreciated Thompson’s take on role-reversals:

“Amazon (media) is trying to become Disney, while Disney is trying to become Netflix.”

Who will be more successful?

Netflix’s magical thinking of making content on a faster paced assembly-line for its 24/7 global platform, or the “Magic Kingdom” showing its mountain of content for its own platform?

Netflix’s drive to create “B” average content (as per Derek Thompson) on a high growth global platform must confront the potential of Disney’s delivering “A” grade content on its own network (plus theme parks and all kinds of merchandising to boot).

II. Value Chains

There are others focused on answering the question about Netflix and Disney. Ben Thompson (no relation to the Derek Thompson I think) of the well-known Stratechery newsletter and his colleague James Allworth of HBS have a Exponent podcast do deep dives on the economics driving tech companies, including the economics underlying Streamland, including Disney and Netflix, and I’m going to do my best to share what I think I learned.

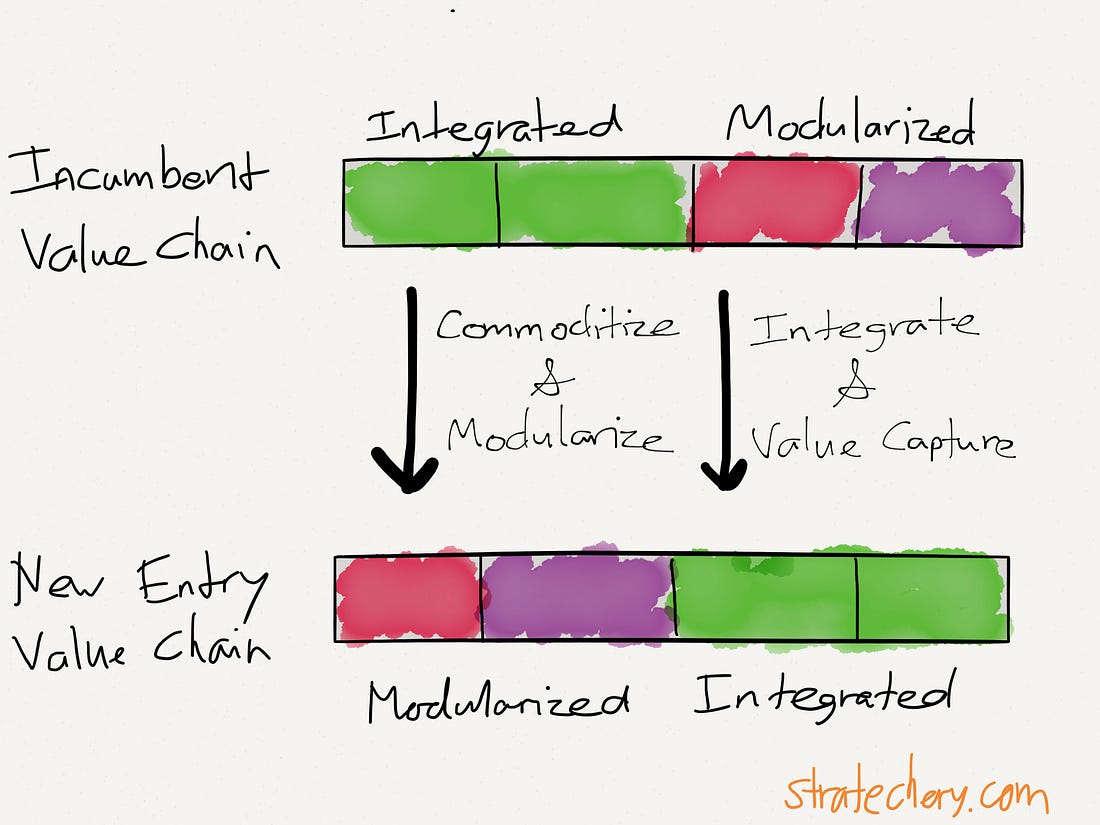

“profits are earned by the integrated provider in a value chain, and that profits shift when another company successfully modularizes the incumbent and integrates another part of the value chain…”

Ben Thompson’s focus on this economic model is relevant for Netflix and Disney. Thompson describes a successful business as an “integrated provider” in a “value chain” enjoying the majority of the profits in the value chain that is until there is change, perhaps from new technology. Such an “integrated provider” holds a position of dominance, a choke-point, and that is where most of the profits accrue. Which modules are integrated can change, which also means a change in incumbents.

When there is such a change a new entrant, such as a start-up or younger/outsider company using the edge of new technology, can come in and “modularize” a pre-existing incumbent. The newcomer can turn an incumbent’s “integrated modules”, where the incumbent held an economic advantage, into commodified ones and takeover as a new dominant business. We recognize this whenever we see examples of “disruption”. Once this happens, the newcomer knocks out an older incumbent from its dominant economic position.

There’s a sketch from Thompson’s Stratechery newsletter which illustrates this model.

As examples, think of IBM’s dominance of computing before Microsoft came along, or Microsoft’s dominance of the PC market until smart mobile phones eclipsed PCs. Or just think of what Netflix did to Blockbuster Video. Thompson’s sketches plus reviewing historical examples has been helpful .

Intel dominated the PC market, as part of “Wintel” with its business model and identity rooted in designing ever faster chips and running foundries to build them. They kept focusing on building smaller and faster chips, and the related modules of software and associate hardware, which might have been slow or bulky were kept running in timely fashion thanks to the horsepower and speed of Intel. Intel held a choke-point as did Microsoft’s Windows OS, hence “Wintel”. The profits and valuation accretted around them.

This changed for “Wintel” when something new came on the scene, changing the focal point for integration of the personal computing value chain, and creating a new chokepoint: mobile smart phones. A demand shift for the more energy efficient left Intel behind. Enter other players who would benefit in the shuffling of modules, including ARM Holdings, with its focus on chip design and licenses, while another player TSMC would be a cost-plus producer to make them.

Ben Thompson: “When integration shifts, profits of modularity shift”.

III. Vertical and Horizontal Businesses:

Some examples to illustrate vertical and horizontal models.

The most prominent vertical business is Apple: which includes its design, contract manufacturing of devices, and media and services sold & delivered under one OS ecosystem.

The most prominent horizontal business is Google: whose strength comes from the scale of reaching as many people on Earth as possible for its search and advertising platform, while funding and providing ancillary services and software for all users.

Let’s bring all of this back to Disney and Netflix.

To oversimplify, Disney can either make a deal and remain what Thompson believes it has always been, a “vertical” platform and double down on remaining as the “Intel” of Grade A content and just focus on design and manufacture. This approach, however, risks an outcome that confronted Intel when the global market for chips changed due to the emergence of mobile smart devices, a/k/a Netflix. So, what if Disney opted instead to leave behind its vertical model roots?

If Disney chooses a “horizontal” model, like Netflix, it might need to change its culture, and “loosen up” on the process of content creation, while also abandoning its old business model, which was quite profitable when cable was the dominant distribution network for its content.

Thompson and Allworth believe a crisis of self-image faces Disney while its business model and pre-internet cable company “edge” have been eroded by the internet and the rise of new entrants, with Netflix at the head of this new cohort.

Disney is not alone in facing this existential crisis.

IV. Cage Match:

Galloway observes that there is a “cage match” going on with Comcast going after Sky to outbid Fox, while Disney is acquiring Fox assets, while Comcast also wants Fox bits too. He likens Old Media to an aged Rocky Balboa, compensating as best as he can by making “bombs” out of his fists, now that he’s older and slower. I appreciate that analogy — an aging champion with failing vision whose reflexes are off needs to compensate with mass.

A business can suffer like Balboa in his sunset years, having lost the ability to see forward and/or stay quick enough to pivot and iterate. Relatively young contenders, NFLX (and Amazon), used to constant forward-thinking reappraisals and reinvention, keep growing monthly subscriber cash and have access to cheap financing due to higher growth rates. Galloway sums up what is to become of the cage match in Streamland:

“I believe the majority of shareholder gains over the next decade will accrete to firms that take the plunge and make bold investments to string together a bundle of assets and offerings that removes friction and convinces the consumer to move in with you. Just as wars are won with logistics and brute force, this battle will be won with cheap capital. Specifically, who has access to the most cheap capital. The cultures of creativity and understanding of how to manage talent give old media a 3–5 year stay of execution….”

I think this scenario is right. Disney does have a deep vertical “culture” of creativity, giving it some time, but 3 to 5 years can go by quickly.

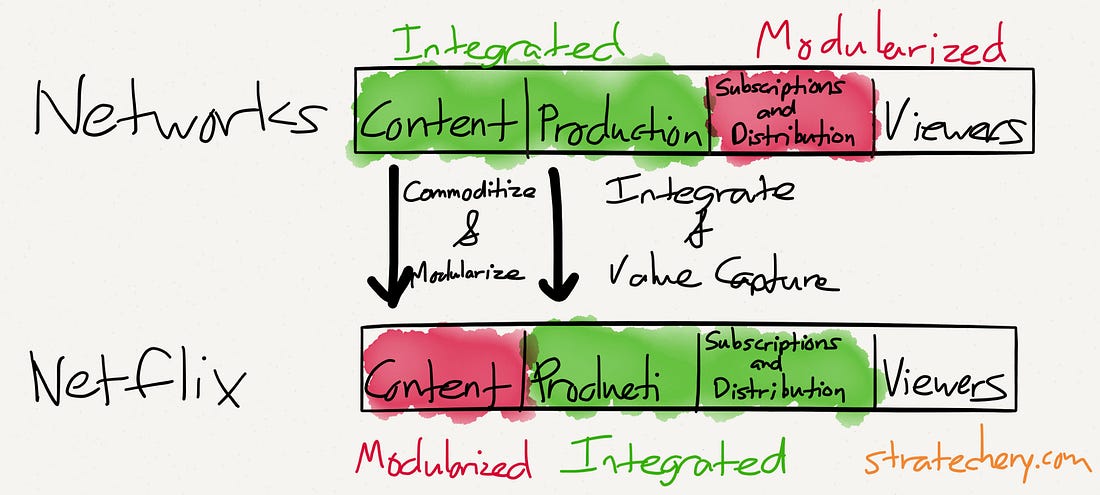

Let’s look at what Disney has realized it’s facing from Netflix with another Stratechery sketch. Recall the “green” of those “integrated modules” in the first “value chain” — where both the economic dominance and profits are made and held initially. Think about every old incumbent business I’ve mentioned like IBM, Microsoft, Intel and it’s no wonder Disney is ending its deal with Netflix.

Notice what happens when a new technology and new business comes in. The second “value chain” in the lower half of the chart shows the change in where the profits will be made by the shifting of which modules are integrated by a new entrant, giving it economic dominance, allowing it to accrete the “majority of shareholder gains” described by Galloway. That would include Netflix.

If you think this is all a bit much, and that Disney is safe, then let’s go to one media industry, which had centuries of profits but has been in crisis: Newspapers.

Newspapers were a bundle of different types of content for different audiences, all integrated, making a fortune from advertising and subscribers. That would all be slowly eroded by “FANG” companies, as described by Ben Thompson, when companies like Google would “modularize” all those newspaper sections and take all those advertisement revenues away. New entrants like Buzzfeed became the “TSMC” of media (size and scale), while newspapers suffered the fate of Intel confronted by the shift to smart mobile phones.

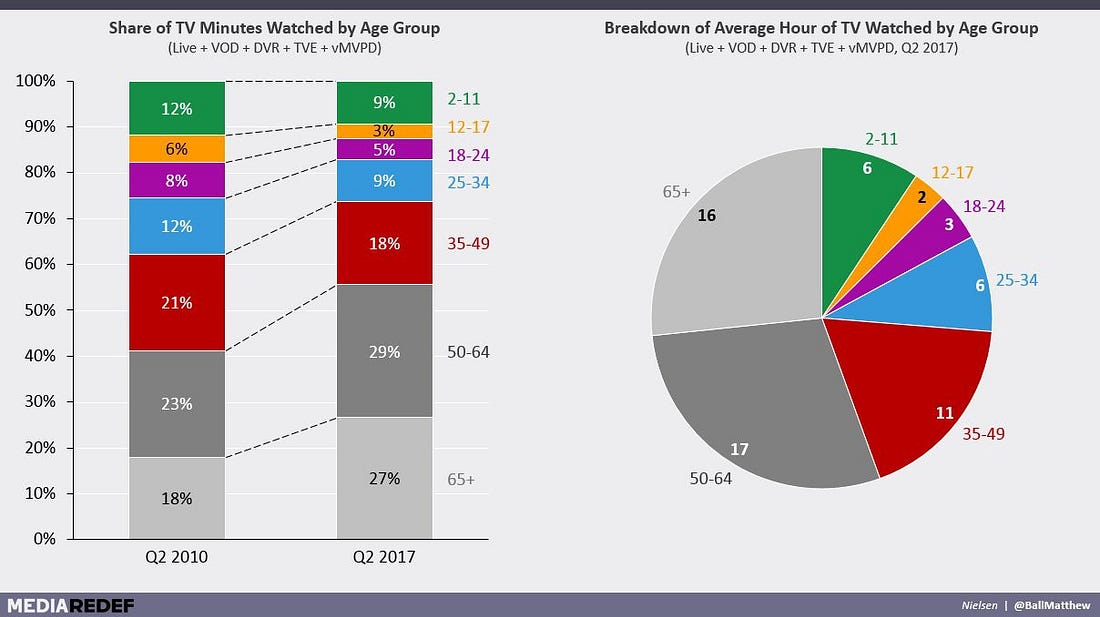

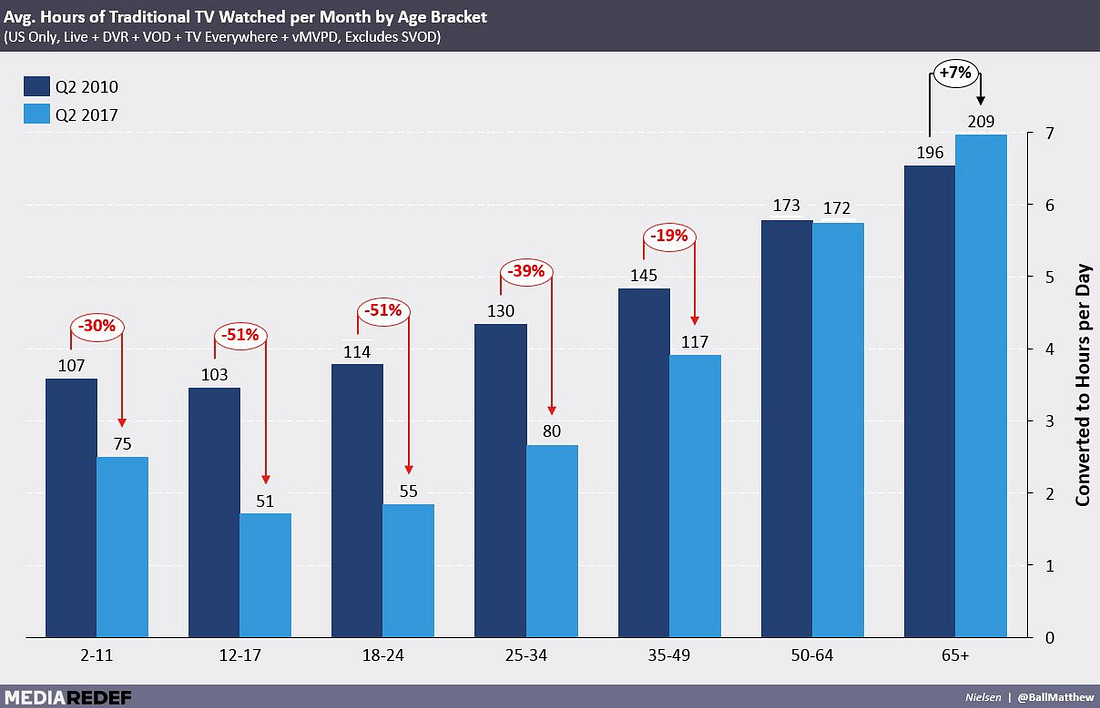

The same thing appears to have happened in television. There has been an undeniable shift in “traditional television” watching habits. The modules have already been reintegrated in favor of new emerging incumbent business model. The audience of the future has moved on away from regular TV.

Disney circa 2023–2025, for its survival’s sake, must by necessity look like a different kind of business under the surface. When Disney made the Netflix deal in 2012, it may have been under the mistaken narrative that Netflix was just another distribution platform like cable. It would take nearly 5 years before their late 2017 awakening that the “chill” and binge-watch platform was a rival poised to eclipse their business model.

Let’s assume that old media bought itself 3 to 5 years via its current model built on creativity and managing talent, atop a vertical money machine. What should they do in the time they have left? They are incumbents confronted by 24/7 platforms with millions of monthly subscribers cutting cords or never signing up for cable TV in the first place. Their horizontal flywheels keep drawing in more subscribers to their platforms, with ever increasing bundles of friction-free assets (on demand, binge 24/7 almost everywhere).

Galloway believes leaders like Iger can pass the existential test facing old media’s culture and self-image and push towards where the dominant integration of modules have shifted to and away from the “wintel” style franchise it had for decades with cable networks.

It is a tantalizing vision for the 2020s: The potential for a “DisneyFlix” horizontal juggernaut, with A+ content, on demand, not to mention merchandising, theme parks and special invitation only venues is enormous. (The content includes the Magic Kingdom’s library, ESPN, Star Wars, Pixar and Marvel.) If the usual movie hits of the likes of Star Wars or Marvel were suddenly available on demand at home not long after theatrical release, this could present a shifting and reintegration of the media value chain’s modules back to Disney’s favor.

Derek Thompson described what a future Disney could become and it wouldn’t JUST be like Netflix: “Disneyflix wouldn’t just be Netflix with Star Wars movies — it would be Amazon for Star Wars pillowcases and Groupon for rides on Star Wars roller coasters and Kayak for the Star Wars suite at Disney hotels.”

If Disney pulls it off, then all it might have to worry about is the same enemy of Netflix: Sleep.

At the moment it appears CEO Iger has begun the work of rebuilding Disney’s business model. The end of Disney’s deal with Netflix nears along with a short-term surrender of revenue during a pivot. This maybe be to a more direct to consumer relationship with differentiated content and higher average revenues per customer. If they are successful with their plans for Fox assets, that means maybe X-men fans will rejoice with a reunion of all the characters from that comic book universe but that’s the cherry on top of the dessert of getting Fox Studios and other content, further expanding the library.

(The funny part is that at the same time Disney is becoming a “Netflix + more” in its own right, Netflix itself has been exploring how it might be little bit more like Disney when it briefly considered buying theaters from Mark Cuban to help promote its in-house produced films.)

V. So What Is Bingewatching Worth?

Disney shares have not enjoyed the multiples of Netflix. I have leaned on and parroted insights shared by Ben and Derek Thompson, Scott Galloway of NYU and James Allworth of HBS. I have one more experts’s work to share regarding Netflix, NYU Prof. Aswath Damodaran. If there is anyone who could provide an unbiased valuation, it would be Prof. Damodaran.

Netflix confirmed that it would be cash flow negative to about 3 to 4 billion in 2018 due to its long game push into making content, having created content “comparable to similarly focused U.S. domestic cable”. It has become so comparable to the point of now having recently made a deal with Comcast to have Netflix bundled in some packages, like its deal with Sky, Proximus and Altice in Europe and T-Mobile in the U.S. It claims the tradeoff is it might get lower fees in return for lower turnover or churn. Some investors might be asking themselves what the leading nation of Streamland is actually worth.

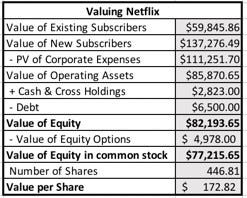

Damodaran provides a valuation lens on Netflix, and offered a recent valuation of about 170+/share — with the caveat that the calculation is an estimate based upon his current interpretation of the reported data and narrative of his assumptions. At this moment that valuation is considerably lower than market quotations. But what if we added another consideration to this estimate?

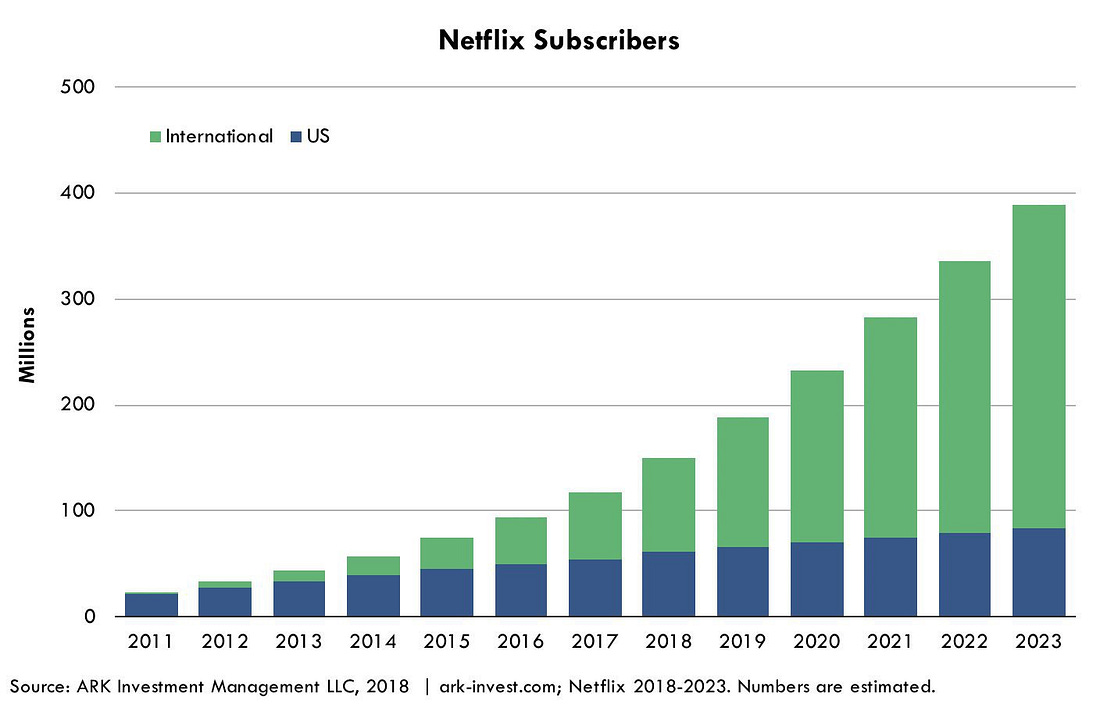

ARK Invest has estimated that Netflix could triple from its current user base to 400 million users in 5 years by 2023 which according to their analysis is double current estimates by other analysts. ARK posits that the company is in the latter half of an “S Curve” growth path, and asserts global growth will be greater due to fixed line broadband expansion. In addition to its infrastructure scenario, ARK contends that the company’s international operations may scale not unlike an early stage growth company ramping up.

The ARK projection is not unreasonable given that the most recent quarterly report cited that 50% of revenue was from international subs, justifying Netflix’s long game investments. A part of that long game includes $1B USD in content deals in over half a dozen European countries, which is just a slice of a planned total $8B spend for 2018 in original and licensed content, and not unreasonable given that about 70+M of the 125M subs are outside the U.S. The subscriber growth projection is at the heart of this analysis.

An observation by Damodaran is that Netflix has steered the conversation and narrative to have everyone focus on subscribers but has cautioned that the current driver of valuation is content creation costs, which the company admits has resulted in substantial negative cash flows. Disney must make a platform and Netflix must deliver on the enormous cash burn on content. The next five years for both companies will be interesting.

Some Chart Art: Disney might be living like its 1999 (as in Netflix at beginning of its long growth arc). Here’s an image of the old Netflix page.

Let’s review a picture of the “cagematch” of all the media players. Random: I make note of the future potential challenge for Disney with its play in HULU given its relationship with Comcast.

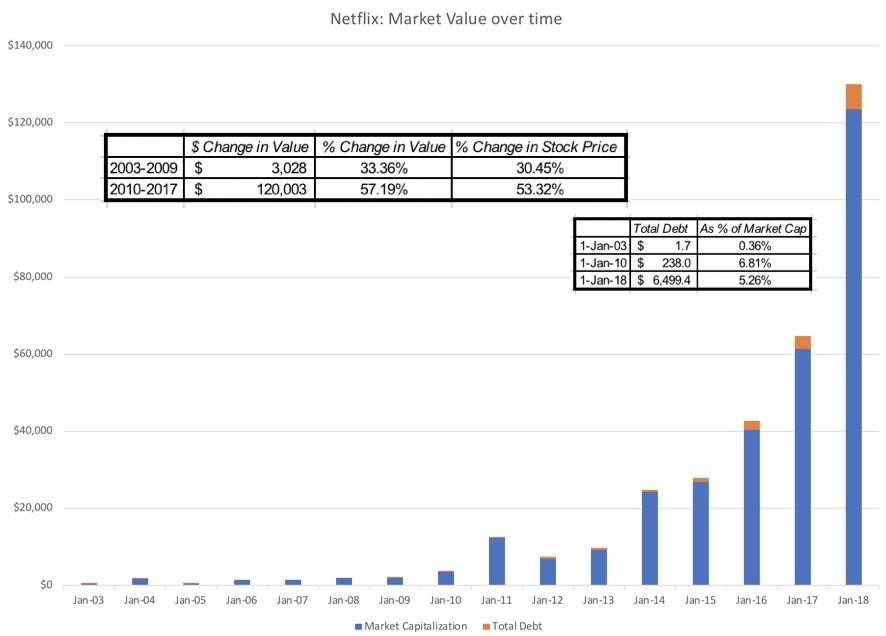

Here are some great charts about Netflix, provided by investment firm Avory & Company.

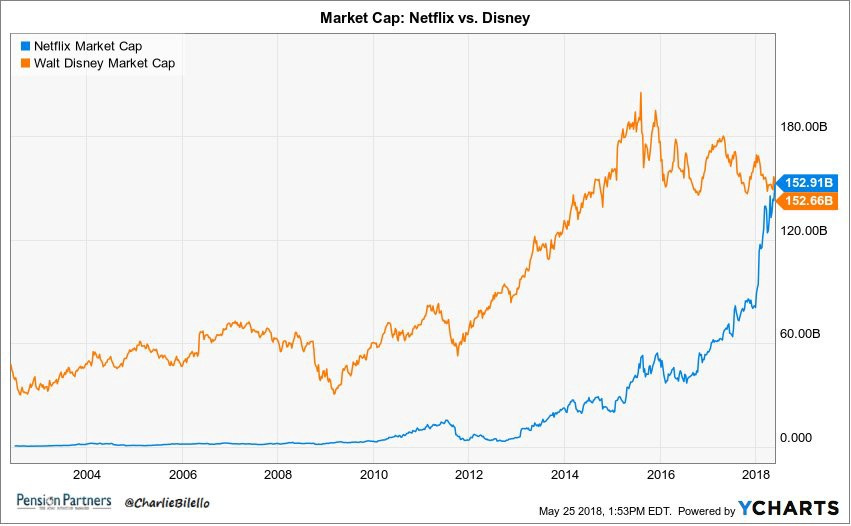

Closing with stock charts for Disney and Netflix. Disney has a long road ahead.

Sources include Ben Thompson’s Stratechery site and his podcast with James Allworth, Prof. Scott Galloway’s interviews and L2 posts, ARK Investment, Avory & Company, Prof. Aswath Damodaran. and Redef. Hopefully, I got the gist of their collective observations and analyses summarized in this piece.

Some links to their work and some incredible deep dives on an exciting topic:

https://stratechery.com/2017/disneys-choice/

https://stratechery.com/concept/business-models/horizontal-versus-vertical/

Aggregation Theory

Aggregation Theory is a completely new way to understand business in the Internet age. Business schools suggest that…stratechery.com

https://redef.com/original/presentation-redef-on-the-future-of-video

http://aswathdamodaran.blogspot.com/2018/04/netflix-future-of-entertainment-or.html

https://ark-invest.com/research/netflix-400-million-subscribers

Disneyflix Is Coming. And Netflix Should Be Scared.

Will Disney destroy the movie theater? No company has been more responsible for shaping the modern entertainment…www.theatlantic.com

More on The Big Stack: The Intersection Between History, Trends & Tech

Originally published at big-stack.com on May 11, 2018.